Veris Economic and Market Update: Q2 2024

Sources: U.S. Bureau of Economic Analysis, FRED, and U.S. Bureau of Labor Statistics³

Consumer Debt Trends

Consumer spending was mostly flat as the bottom 80% of households have depleted most of their excess savings and are taking on more debt. The household debt service ratio increased from 8.3% in March 2021 to 9.8% in June 2024.⁴ As the unemployment rate rises, delinquency and default rates are expected to rise at a faster pace across all consumer loans. After reaching historical lows in Q2 2021, credit card delinquency rates have been steadily increasing and have surpassed pre-pandemic levels.⁵ Higher delinquency rates will likely further hinder credit availability and result in decreased consumer spending.

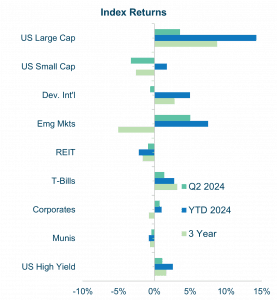

Q2 Market Activity

Q2 Market Activity

Q2 Market Activity

Q2 Market ActivityPublic equity markets had mixed returns in Q2 as high inflation in April sent stocks falling but improving inflation data bolstered the stock market by the end of the quarter. US Large Cap benefited from gains in the mega cap tech stock as market exuberance about artificial intelligence (AI) continued to dominate. Emerging Markets generated relatively outsized positive returns in Q2 driven by Taiwan which benefited from the AI theme and supportive policy measures from China. Strong economic data from India also helped. Bond markets generally had positive returns as investors anticipated the Fed will cut rates in the second half of 2024.

Sources: Morningstar Quarterly Index Returns Report, FRED, and US Department of the Treasury⁶

S&P 500 “Magnificent Seven to Magnificent Five”

Seven US large-cap companies – Microsoft, Apple, Nvidia, Meta, Amazon, Tesla, and Alphabet – were responsible for more than half of the gains in 2023 but are more dispersed in 2024, with Nvidia and Meta leading and Tesla and Apple lagging. Despite that, the “Magnificent Seven” represented ~32% of the S&P 500 Index weight and accounted for ~61% of the S&P 500 Index YTD returns. Nvidia rose ~150% contributing to 30% of the gains in the S&P 500 in 2024. Actively managed portfolios without exposure to these companies, particularly Nvidia, have trailed their benchmarks in recent years and concentration risk is severely elevated in passively managed portfolios with exposure to the Magnificent Seven.

Source: Morningstar, J.P. Morgan Asset Management⁷

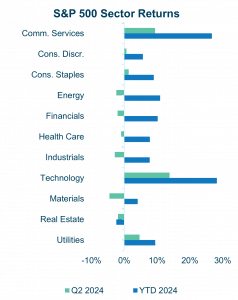

Stock Market Update – Sector Focus

Stock Market Update – Sector Focus

Stock Market Update – Sector FocusTechnology, Communication Services, and Utilities had the strongest returns in Q2, but these sectors mask some striking trends. Artificial intelligence has propelled stocks since late 2022, and the second quarter of 2024 was no different. Within the S&P 500, companies related to the theme gained 14.7% in market value this past quarter, whereas the rest lost 1.2%. Six out of 11 sectors – healthcare, real estate, financials, energy, industrials and materials – lost market value.

Source: Morningstar Quarterly Index Returns Report, S&P Global, MSCI⁸

What Will the Fed Do? Economic Indicators to Pay Attention To

Along with volatility stemming from the concentration of market returns from a very small number of stocks, markets over the last year have reacted to expectations of actions by the Federal Reserve that have not come to be. At the end of 2023 market consensus was that the Fed would reduce interest rates 3 times in 2024.⁹ Meetings in the first half of the year came and went with no rate cuts and little signaling by the Fed of imminent rate cuts as inflation remains above the Fed’s target and the labor market remains strong despite some softening. As we examine market volatility and what may lie in the months ahead, it may help us to understand more about economic indicators and their relationship to market expectation. In looking at the economy and its relationship to market volatility, there are three economic indicators we want to understand:

- Economic growth as measured by GDP.

- Inflation as measured by the Consumer Price Index (CPI) and Producer Price Index (PPI).

- Unemployment – measured primarily by the unemployment rate.