Economic & Market Update: Q3 2024

By Jane Swan, CFA and Roraj Pradhananga, CIMA & CPA

As we write, the 2024 general election in the United States is less than two weeks away, and values-aligned investors are keenly aware of the social and environmental issues that are on the line. With this letter, we aim to put the economy and markets in context of the upcoming election, and to put this election in some historical context as well.

The US economy continues to remain resilient. In the second quarter the economy grew at an annualized rate of 3%, accelerating from an upwardly revised 1.6% expansion in the first quarter. This is in line with the 3% year-over-year GDP growth as strong consumer spending driven by a resilient labor market and wage growth continues to support the US economy. Inflation pressures continued to ease, allowing the Federal Reserve greater confidence to shift their primary focus from lowering inflation to supporting the labor market. In September, they lowered interest rates by 50 bps (0.5%), making the first rate cut in four years.

Sources: U.S. Bureau of Economic Analysis, FRED, and U.S. Bureau of Labor Statistics 1

The Federal Reserve was supported in this rate cut by inflation’s continued trending downward, though slower than economists had forecasted. September headline Consumer Price Index (CPI) was 2.4% vs. expectations of 2.3%. Core CPI, which excludes volatile food and energy prices, remained steady at 3.3%, slightly higher than the 3.2% rise in August. While inflation continues to ease, it remains above the Federal Reserve’s 2% target, with food and shelter costs the two major contributors. Shelter inflation, which is a significant component of core CPI at 37%, continues to trend downward. Motor vehicle insurance, though a smaller component of the overall reading, is up significantly at 16.3% year over year. While home insurance is not a component of CPI, the increase in climate related extreme weather events is impacting the price and availability of home insurance in states including California and Florida. 2

Source: Bureau of Labor Statistics 3

Labor Market

The US labor market shows continued strength as job growth in September topped all estimates. The unemployment rate unexpectedly declined, and wage growth accelerated. Non-farm payrolls increased 254,000 in September, the most in six months, following an upwardly revised increase of 72,000 jobs over the prior two months. The unemployment rate fell to 4.1% and hourly earnings increased 4% from a year earlier. Unemployment rates were down across all races, with Black Americans experiencing the biggest decrease from 6.7% in June to 5.4% in September.

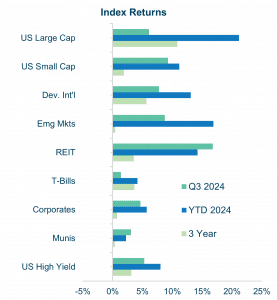

We often remark that the stock market does not like uncertainty. The market does not seem to be fazed by the uncertainty many of us are feeling about the election. US equities continued to build on a strong start to the year, with many market indices nearing record highs in Q3 as investors remain very optimistic. The rally has reacted positively to the Fed interest rate cut and strong GDP growth, and companies’ revenue and earnings growth continue to beat expectations. Public equity markets experienced solid returns, led by US Small Caps at 9.3% while the Russell 1000 was up 6.1%. Emerging Markets also posted stronger returns in Q3, driven by new stimulus measures in China as well as the Federal Reserve’s interest rate cut. Bond markets generally had positive returns as yields decreased across the board. However, market participants are expecting multiple rate cuts in Q4, but the Fed remains data dependent and stronger than expected inflation or labor market reading will influence the FOMC’s decision. The FOMC’s decision that diverges from market expectations can impact bond yields and hence prices of bonds.

We often remark that the stock market does not like uncertainty. The market does not seem to be fazed by the uncertainty many of us are feeling about the election. US equities continued to build on a strong start to the year, with many market indices nearing record highs in Q3 as investors remain very optimistic. The rally has reacted positively to the Fed interest rate cut and strong GDP growth, and companies’ revenue and earnings growth continue to beat expectations. Public equity markets experienced solid returns, led by US Small Caps at 9.3% while the Russell 1000 was up 6.1%. Emerging Markets also posted stronger returns in Q3, driven by new stimulus measures in China as well as the Federal Reserve’s interest rate cut. Bond markets generally had positive returns as yields decreased across the board. However, market participants are expecting multiple rate cuts in Q4, but the Fed remains data dependent and stronger than expected inflation or labor market reading will influence the FOMC’s decision. The FOMC’s decision that diverges from market expectations can impact bond yields and hence prices of bonds.

Sources: Morningstar Quarterly Index Returns Report, FRED 7

The Magnificent Seven

The seven US large-cap companies referred to as the “Magnificent Seven”– Microsoft, Apple, Nvidia, Meta, Amazon, Tesla, and Alphabet – were responsible for more than half of the gains in 2023 but are more dispersed in 2024. Nvidia and Meta led the pack while Tesla and Microsoft lagged. Despite that, the “Magnificent Seven” represented approximately 31% of the S&P 500 Index weight and accounted for roughly 45% of the S&P 500 Index YTD returns. Nvidia has risen over 145% contributing to 20% of the gains in the S&P 500 in 2024. Many actively managed portfolios without exposure to these companies, particularly Nvidia, have trailed their benchmarks in recent years. Concentration risk is elevated in portfolios with market exposure or overweights to the Magnificent Seven.

Sources: Morningstar, JP Morgan Asset Management 8

Sector Trends

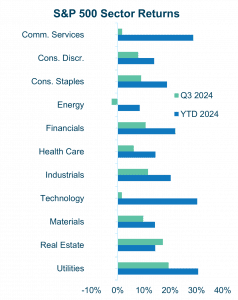

Utilities, Real Estate, and Industrials sectors emerged as the top performers in the quarter, each benefitting from the anticipated Federal Reserve rate cuts. The Utilities sector received an additional boost from heightened electricity demand attributed to data centers supporting the artificial intelligence (AI) expansion. Utilities have a key role to play in the energy transition and the shift to renewable energy from fossil fuels is even more relevant today due to increased demand. A notable shift occurred as investors rotated out of large-cap technology stocks and into value and small-cap equities leading to the Technology and Communication Services lagging the broader market. Energy was the only sector with negative returns for the quarter, largely due to falling crude oil prices driven by lower demand and increased supply.

Utilities, Real Estate, and Industrials sectors emerged as the top performers in the quarter, each benefitting from the anticipated Federal Reserve rate cuts. The Utilities sector received an additional boost from heightened electricity demand attributed to data centers supporting the artificial intelligence (AI) expansion. Utilities have a key role to play in the energy transition and the shift to renewable energy from fossil fuels is even more relevant today due to increased demand. A notable shift occurred as investors rotated out of large-cap technology stocks and into value and small-cap equities leading to the Technology and Communication Services lagging the broader market. Energy was the only sector with negative returns for the quarter, largely due to falling crude oil prices driven by lower demand and increased supply.

Sources: Morningstar Quarterly Index Returns Report, S&P Global, MSCI 9

How Might the US Election Influence Markets? We Look to the Future Guided by Insights from the Past

Investors may be concerned about the impact of the presidential election on markets due to the uncertainty of changes to regulations, tax and trade policies, fiscal spending, etc. Volatility as indicated by the CBOE Volatility Index (VIX) is usually elevated in the months leading up to the presidential elections. 10

Despite the volatility, US equities have historically performed well after election years. Particularly of note is the positive equity market returns 6 months after the election. The actualization of any policy proposals will depend on election outcomes for not just the presidency, but also the results of elections determining control of the House and the Senate.

Source: Bloomberg 11

Note: Data represents the average return six-months before and after the past seven U.S. presidential elections (1996 – 2020)

An Annotated Calendar of Important Post Election Events Investors Should Pay Attention To

No one knows what the final outcome may be, but we do know the exact dates of noteworthy events related to the election that investors may want to pay close attention to, including:

- November 5, 2024: Election Day. We expect that it may take several days for the results to be determined.

- December 20, 2024: Expiration of short-term spending deal. Congress will either need to pass another extension or complete an annual budget for President Biden’s signature. 12

- January 2, 2025: Federal debt ceiling will be reinstated. The debt ceiling was suspended on June 2, 2024. Once reinstated, the ceiling will need to be raised to permit ongoing spending. There will be some window of time where the Treasury Department will use “extraordinary measures” to continue spending for a limited period while Congress works out a deal. The unknown but limited time-period is referred to as the “X-date.”

- January 6, 2025: Certification of election results. Through the majority of US history, this has been an uneventful day.

- January 20, 2025: Inauguration Day. The market may express relief for the conclusion of this contentious election.

- Early to Mid-2025: Expectations for exhausting those extraordinary measures range from spring to summer. If Congress does not reach a deal within the powers of those extraordinary measures, there could be a government shutdown.

While we do not expect any of these events to be a catalyst for a specific market outcome, we recommend considering expected spending needs and accounting for spending through cash and liquid reserves. Aside from allocating to cover expected spending needs, we recommend clients remain invested despite the uncertainty and heightened potential for volatility. Your Veris Advisors are available to help you plan for the years ahead.

For more recent insights, read The Q1 2025 Economic and Market Update.

Sources

1 U.S. Bureau of Economic Analysis, FRED, and U.S. Bureau of Labor Statistics

2 nytimes.com/interactive/2024/05/13/climate/insurance-homes-climate-change-weather.html

3 Bureau of Labor Statistics

4 U.S. Bureau of Economic Analysis, FRED, and U.S. Bureau of Labor Statistics

5 reuters.com/markets/us/us-retail-sales-increase-solidly-september-2024-10-17/

6 FRED and Federal Reserve Bank of Philadelphia

7 Morningstar Quarterly Index Returns Report, FRED

8 Morningstar, JP Morgan Asset Management

9 Morningstar Quarterly Index Returns Report, S&P Global, MSCI

10 www.cboe.com/tradable_products/vix/

11 Bloomberg

Disclaimer

The information contained herein is provided for informational purposes only and should not be construed as the provision of personalized investment advice, or an offer to sell or the solicitation of any offer to buy any securities. Rather, the contents including, without limitation, any forecasts, projections, and forward-looking statements simply reflect the opinions and views of the authors.

All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change without notice. There is no guarantee that the views and opinions expressed herein will come to pass. Additionally, this document contains information derived from third party sources. Although we believe these third-party sources to be reliable, we make no representations as to the accuracy or completeness of any information derived from such third party sources and take no responsibility therefore. Information related to the performance of certain benchmark indices is provided for illustrative purposes only as investors cannot invest directly in an index. Past performance is not indicative of or a guarantee of future results. Investing involves risk, including the potential loss of all amounts invested.