How Climate Change Caused PG&E’s Bankruptcy

Veris Guest Blog: By Timothy P. Dunn, CFA

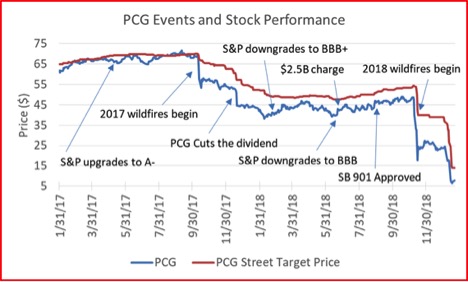

Pacific Gas & Electric (PG&E) Corporation, California’s largest investor-owned utility, which serves roughly 5.2 million households in central and northern California, filed for bankruptcy and is facing an estimated $30 billion of potential liabilities stemming from its equipment’s role in the historic 2017 and 2018 wildfires.

PG&E’s bankruptcy is indicative of how our changing climate presents real economic and financial risks for companies and investors. Prior to the wildfires that burned over 240,000 acres, PG&E included warnings that weather-related disasters could weigh on or disrupt its operations in its regulatory filings. In a statement, the company noted that the state’s most recent climate assessment “found the average area burned statewide would increase 77 percent if greenhouse gas emissions continue to rise,” and that “prolonged drought and higher temperatures will triple the frequency of wildfires.” Further, PG&E performed extensive water risk assessments, water management was integrated into its business strategy, and the company spent hundreds of millions of dollars every year in fire prevention, including pruning or removing thousands of trees. This awareness and action, though necessary and important, was not enough.

In an environment that continues to be challenged by climate change, PG&E’s situation could be a harbinger of the economic toll of spatially-related climate risk. “California is now a riskier place to do business,” said the Environmental Defense Fund’s Michael Colvin, a former adviser to the California Public Utilities Commission. “This is a statewide problem.”

The bankruptcy not only points out the danger that warming poses for many companies, it also underscores how difficult it is for investors to analyze risks linked to climate change compared to conventional business challenges. It is becoming increasingly clear that economic damage from climate change will affect a variety of sectors, and even companies regarded as forward-thinking might not be able to directly prepare for all the externalities associated with this systemic global problem.

Source: Seeking Alpha

Terra Alpha first purchased PG&E in 2015 based on the fact that it was a leading US regulated power provider with solid fundamentals and a strong record of shifting to lower carbon power generation. Nearly 80% of the electricity that PG&E delivered in 2017 was a combination of renewable and GHG free. Accordingly, PG&E was well-positioned to benefit from increased regulatory action in California aimed at furthering the shift toward renewable energy.

We sold our shares of PG&E in mid-October of 2017, after PG&E’s equipment was linked to the start of several wildfires. We had determined that the risk profile for the stock had dramatically worsened and it was no longer prudent to own. We felt that its exposure to such enormous liability, coupled with CEO Geisha Williams’ concerns about the growing financial risk for PG&E from forest fires, intensified by a changing climate, and California’s unique inverse condemnation laws, represented material undiscounted financial risk.

While PG&E may represent the first climate change bankruptcy it likely won’t be the last. Investors need to learn how to account for long-tail climate risk in their portfolios.

Timothy P. Dunn, CFA, is Founder, Managing Member and Chief Investment Officer of Terra Alpha Investments, LLC, a global equities asset manager.

*The information presented by Mr. Dunn is not an endorsement of Terra Alpha Investments by Veris Wealth Partners.