Economic Update Q4 2016

By Jane Swan, CFA, Senior Wealth Manager

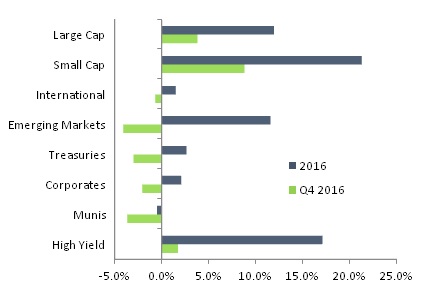

As the market adjusts and tries to make sense of the results of the U.S. election, financial markets have been mixed. After an initial decline in futures markets on election night, the S&P 500 (U.S. large cap) rose 3.8 percent in the quarter, bringing total return for the year to 12.0 percent. The Russell 2000 index (U.S. small cap) had another strong quarter and was up 8.8 percent for the quarter, or 21.3 percent for the year. International markets were less enthusiastic. The MSCI EAFE (developed international markets) slid 0.7 percent for the quarter, bringing year-to-date to a positive 1.5 percent. Emerging markets, the best performing asset class of the prior quarter, were down 4.1 percent in the final quarter, but were up 11.6 percent for the year.

2016 Q4 Asset Class Returns

PMC Capital Markets Flash Report for periods ending Dec 31, 2016

Investment grade domestic fixed-income markets, which had rallied in the prior quarter, gave back much of their gains. U.S. Treasuries returned a negative 3.0 percent in the quarter, driving down year-to-date returns to a positive 2.7 percent. Corporate bonds fell 2.1 percent for the quarter, but up 2.1 percent year-to-date. Municipal bonds were down 3.7 percent for the quarter and 0.5 percent for the year-to-date. Excluding investment grade issues, high-yield bonds finished the year up 1.8 percent for the quarter and 17.1 percent for the year.

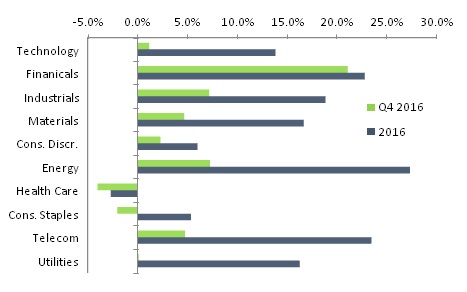

Within the large cap market, the sectors potentially benefitting from deregulation saw the largest gains. The biggest winners: Financials (up 21.1 percent for the quarter, 22.8 percent for the year), Energy (up 7.3 percent for the quarter, 27.4 percent for the year) and Industrials (7.2 percent for the quarter, 18.9 percent for the year). Not far behind were Telecom (4.8 percent for the quarter and 23.5 percent for the year) and Materials (4.7 percent for the quarter and 16.7 percent for the year). Each of these sectors have seen progress on environmental or consumer protection regulations in the last eight years. The market suggests that profits have the potential to be higher (at least in the short term) with less government regulation.

Weaker returns came from sectors mostly thought to have less potential benefit from deregulation. These include Consumer Discretionary (up 2.3 percent for the quarter, 6 percent for the year), Technology (up 1.2 percent for the quarter, 13.9 percent for the year) and Consumer Staples (down 2 percent for the quarter but up 5.4 percent for the year. Utilities had almost no change in the fourth quarter after three strong quarters in 2016. They were up just 0.1 percent in the quarter but 16.3 percent for the year. The worst performance came from Health Care sector, which was down 4 percent in the quarter and 2.7 percent for the year. The uncertainty over the fate of the Affordable Care Act triggered uncertainty about profits for the sector.

2016 Q4 Sector Returns

PMC Capital Markets Flash Report for periods ending Dec 31, 2016

Looking Ahead

With a new administration now in place, we look at each sector to understand how markets may be affected by both political and economic forces. The energy sector, heavily impacted by oil-related businesses, is an instructive place to start.

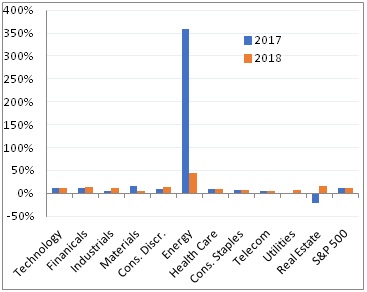

The significant rebound in energy stocks last year happened despite dramatic a year-over-year decline in the sector’s earnings (currently estimated at -66%). Because stock prices tend to express expectations of future earnings, the rise in stock prices is a reflection of the expected significant increase in earnings for companies in the energy sector. The chart below shows current earnings growth forecasts for each sector over the next two calendar years. The estimates for extraordinary forecasted growth in earnings within the energy sector stand out. They are expected to exceed 350 percent. In fact, the forecasted earnings growth has little to do with potential policy or regulation changes under the Trump presidency. The 2017 forecast has changed very little from its pre-election forecast from September 30, 2016.

The anticipated increase in oil stock earnings is instead tied to the expectation that oil will to rise to about $56 by the third quarter of 2017 from a low of $33.69 in the first quarter of 2016. This forecasted increase is expected to boost energy sector earnings from $4.3 billion in the third quarter of 2016 to $14.0 billion in the third quarter of 2017. The price of energy stocks today factor in these expectations. Changes to these expectations, either positive or negative surprises, could further impact the returns of energy stocks. It is important to note that while the current value of energy stocks appears very positive that: 1) globally the majority of new electric generating capacity is solar and 2) grid parity prices for solar and wind are now below fossil fuels throughout Developing world and will at parity in the U.S. over the next 5 years. Finally Bloomberg’s analysis tags 2020 as the year oil consumption peaks globally. These are amazing transformations that are not turning back.

Earnings Growth Forecasts by Sector

FactSet Earnings Insight, January 13, 2017

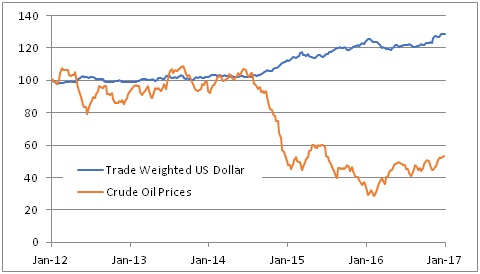

The price of oil is a function of many factors. One key variable is the value of the dollar. (Oil is priced in US dollars.) When the dollar is strong, it weakens the price of oil. An unanticipated change in the strength of the dollar could have a meaningful impact on the current earnings forecasts. Changes to fiscal and monetary policy, as have been hinted at by the incoming administration, could also impact the strength of the dollar.

Oil Prices vs. Strength of Dollar

Board of Governors of the Federal Reserve System (US), Trade Weighted U.S. Dollar Index: Broad [TWEXB], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/TWEXB, January 18, 2017.

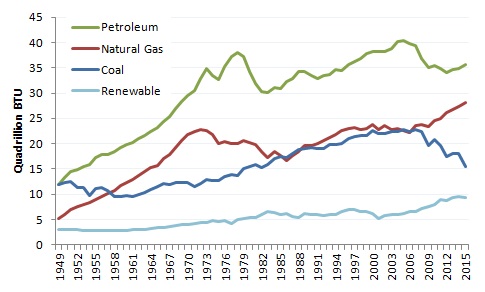

Primary U.S. Energy Consumption by Source

U.S. Energy Information Administration

The impact of tax incentives proposed by the new administration and Congress are uncertain at best. This may not change the business case for renewable. As oil gets more expensive, the interest in sourcing energy from natural gas and renewable energy would be expected to rise. When oil is relatively cheap, as it has been, tax incentives have helped make the financial case for investment in renewable. Moreover, 365 U.S. companies made urged the president-elect to continue participation in the Paris climate deal, citing the business and job creation aspects of climate protection economies. While short-term returns may be volatile and unpredictable for the next few years, there remains a long-term business case for ongoing investments in renewables.

As we look to the broader economy, Veris’ areas of thematic impact focus, and at vulnerable communities, we see important roles for city and state governments, impact investing and philanthropy. Cities and states continue to lead in raising the bar in areas ranging from increasing the minimum wage to addressing climate change. Shareholder advocacy and active investing can replace some of what may be lost by decreased government regulation. Investment in sustainable businesses can address climate change and building healthy communities. With many non-profits relying on government grants for significant portions of their annual budgets, increased reliance on philanthropy is expected. Clearly in this transition in Washington we see the importance of redoubling the effectiveness of impact investing strategies. And we need to remember that for the last 20 years we have collectively been changing the face of business and finance for the better. Impact investing plays an ever bigger role. We appreciate our opportunity to engage in this work with each of you.